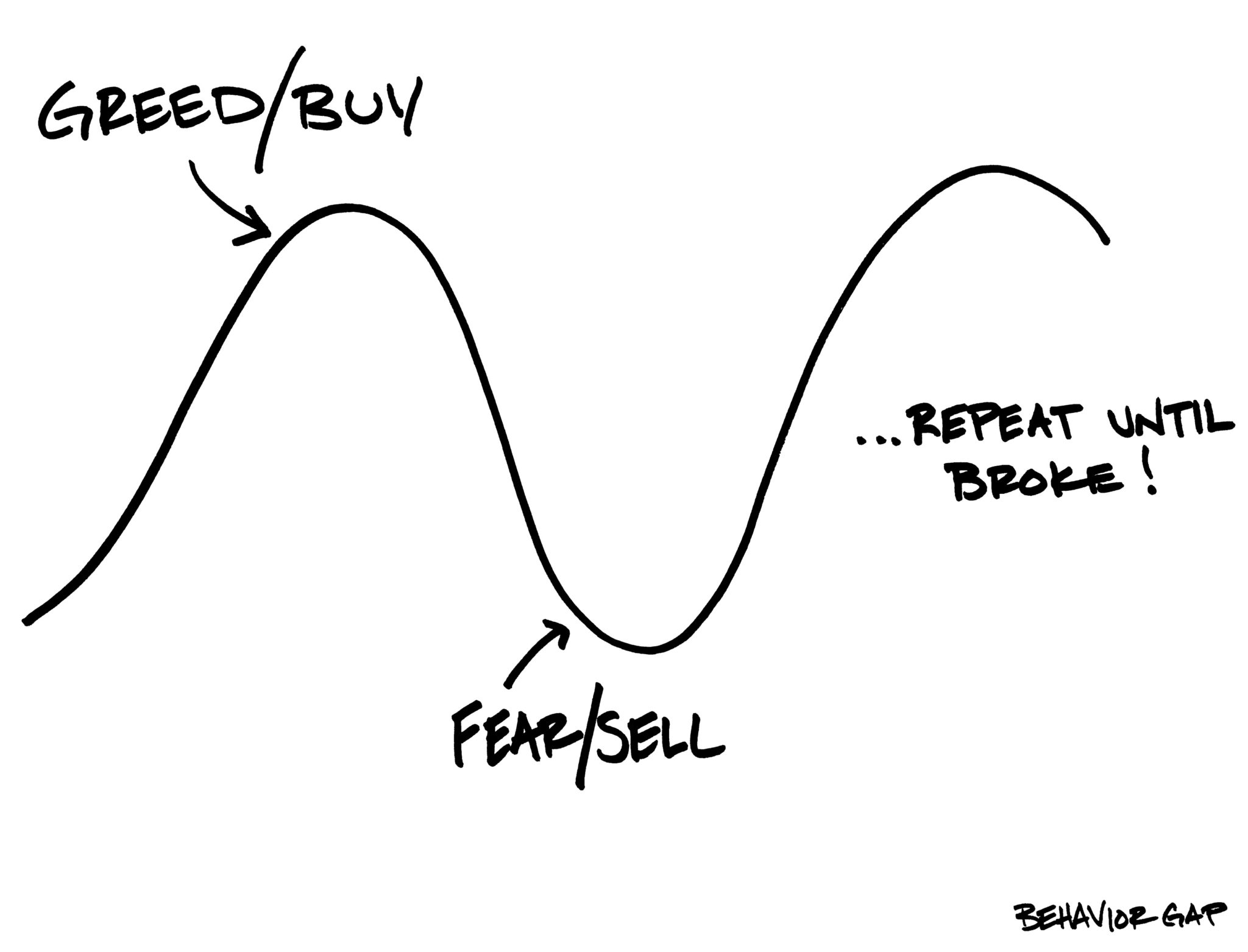

Stock markets were stable to up today, trying to digest the news from the Middle East. It’s my opinion that we are facing many years of instability in the Middle East and elsewhere. The United States has failed to play to win again, even with Trump at the helm.

I don’t care about the politics, but the current reality on the ground shakes my fundamental belief in the US economy. What we see in the news is a lot of “micro” reporting, very little in the way of looking at the long game and how this is going to play out over the years to come.

I cannot imagine what the Taiwanese are thinking right now, how all this will play out for them vis-à-vis the Chinese. I don’t think it looks good. If one were to incorporate this kind of thinking into their investments, how would one adjust one’s portfolio to this “new reality”?

To find a defensive strategy here for someone in my position (74 years old and looking at not so many years to go), there aren’t a lot of good options. Stocks, perhaps. And then I add in my uncertainty around the US Estate Tax if I’m outside of Canada, and my investment options become even more restricted. There is always the option of simply putting my cash into short-term vehicles like treasury bills and treasury bonds. The Investment professionals seem to feel that it is folly.

Not that they offer any viable alternatives. What I do believe is that investors probably don’t rigorously try to determine what their financial needs will be in the future. If you save for retirement, should you not get to a point where you have a target rate of return? Do I need 10% compunded every year to live? This requires some thorough analysis and an honest look at how you can live given what you have got. It’s a simple spreadsheet that most can do with little effort. Analyzing what comes in versus what goes out. Building in a rate of return and your taxes, and voila! Be honest with yourself while looking at what you have versus what you need. Make your lifestyle fit your cash flow.

As I get older, I find I need less, want less and can easily spend less. I don’t have the energy or desire to travel. I don’t spend much as I don’t go out much. I’m too exhausted.

Get real. Have a reasonable plan and move forward.