Markets continue to climb up as I monitor my own behaviour. I bought shares in a small solar technology company that is based in Japan. I happened to read about it in one of the online tip sheets that are so prevalent now. I reviewed the company’s financial statements, which are a complete mess. There’s a whole lot of “creative financing” which is almost impossible for the normal reader of financial statements to comprehend.

I searched around and found a YouTube video the company had posted, and saw the most amazing factory manufacturing solar panels with no people working in it. I decided to purchase the stock even though it had a market cap of less than half a billion dollars. A microcap nowadays.

In the following months, the company announced expansion in the United States to avoid tariffs. The stock skyrocketed.

What’s the point of all this? Now I’m sitting on a large percentage profit. The stock is very volatile, moving 6 or 7 percent a day, some back-to-back days. I cannot decide whether to sell or hold. The gain is enough to be noticeable if the company gets wiped out. A lack of a decision-making tool is the problem yet again. How to decide? If I had set a target profit, I likely would have sold out a long time ago.

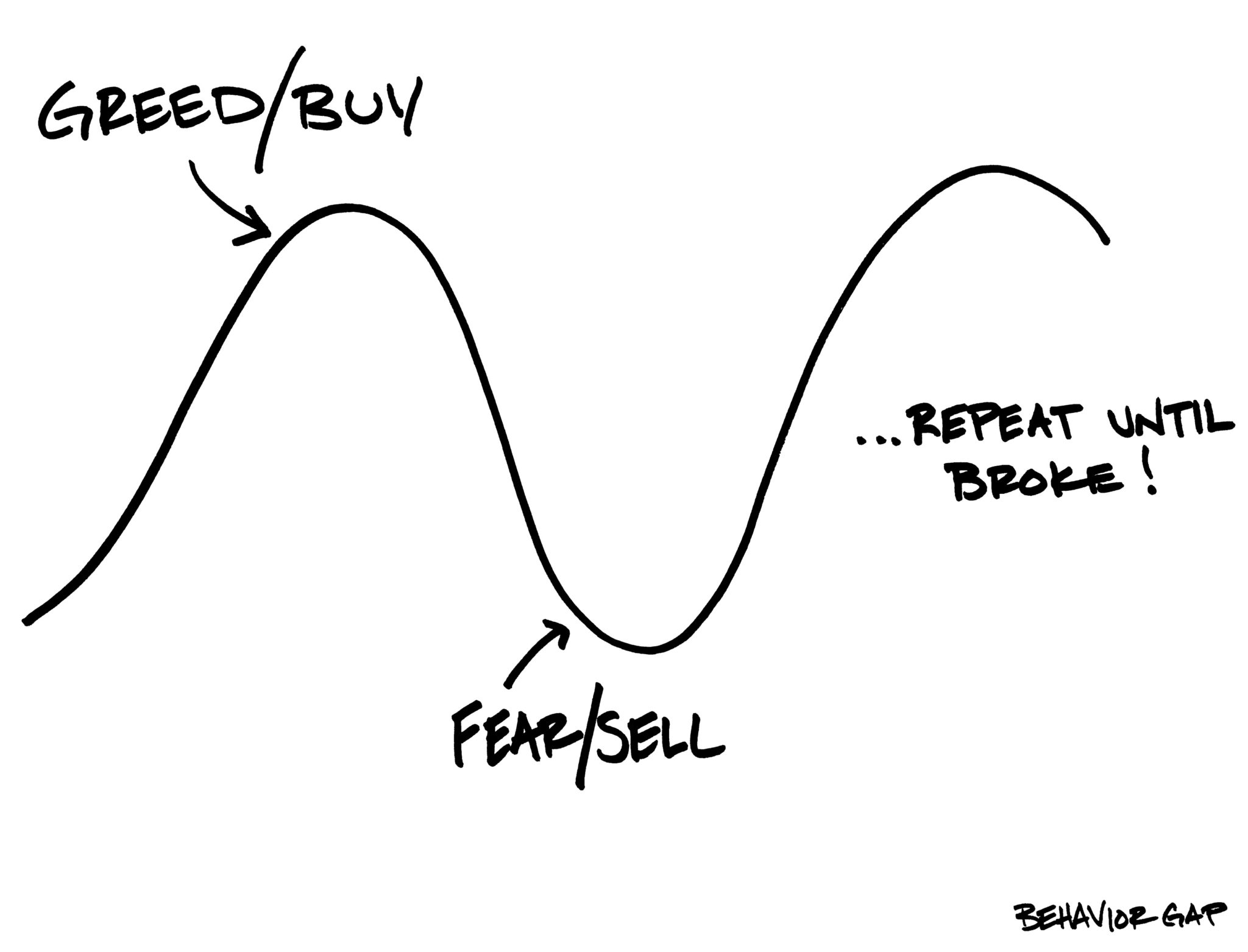

Success in investing is not just about picking the right stock. It’s about making decisions and moving on. When is it enough? I am locked into a vicious circle of both greed and fear. Horrible. How to get out?