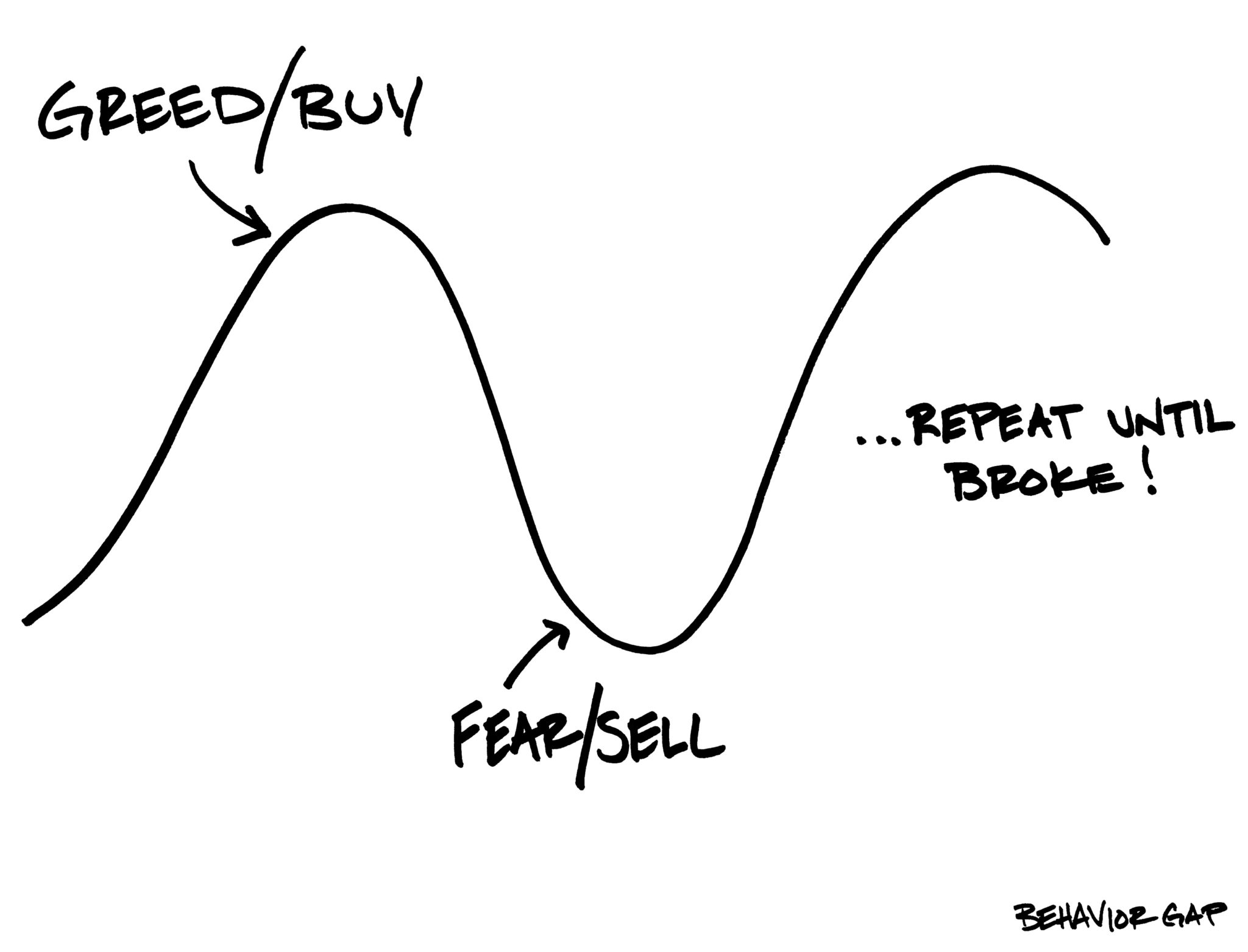

The markets closed on a bit of a sour note today. It seems that the Middle East situation continues to display volatility. I had a bit of government chasing around to do (driver’s license), and it took hours with some missteps. I find the level of compliance now astounding.

More government interference:

“In Ontario, licensing to build new homes is mandatory and regulated by the Home Construction Regulatory Authority (HCRA). It is illegal to build or sell a new home without a valid HCRA licence.

1. Licensing Requirements & Process (HCRA)To obtain a license, you must prove you have the technical and business competence to build homes. Competency Requirements: You or a “Designated Person” in your company must complete seven HCRA-approved education courses.Application & Vetting: You must apply through the HCRA Builder Portal, which involves an audit of your business ethics and financial health.Background Checks: Criminal record checks for directors are required.Tarion Registration: After getting a license, you must register with Tarion Warranty Corporation for the Qualification for Enrolment (QFE) to enroll every new home you build.

2. Licensing Costs (2026)The initial investment to become a licensed builder is significant, with costs split between training, application fees, and security deposits. Mandatory Education: Approx. $4,500 ($600–$670 per course).HCRA License Fee:$3,525 for a new standalone license (no prior history).$880 for a new license tied to an existing “umbrella” group.Renewal Fee: $715 (annual).Tarion Initial Security Deposit: Often a Letter of Credit starting at $10,000+.Professional Fees (CPA/Legal): $500–$2,000 for financial statements.Total Estimated Initial Cost: ~$19,525+.

3. Costs to Build Housing in Ontario (2026). Beyond licensing, the cost to build a house in Ontario is generally between $300 to $600+ per square foot, depending on design, materials, and location. Hard Costs (Labour/Materials): The average cost for a custom home is roughly $340–$575 per sq. ft. in 2026, excluding land.Soft Costs (Permits/Admin): Permits and regulatory fees can add $10,000 to $30,000 or more per project.Location Impact: High-demand areas like Toronto or Ottawa can exceed $400–$500 per sq. ft., whereas rural areas may be cheaper.”

How did we manage to get along without this for all of these decades? It’s just another tax, another barrier to home construction that will reduce housing availability and increase the cost.

Invest in Canada, where you have a business-friendly environment!