I’ve been away for a week, preoccupied by other things. The last week has seen a lot of activity on the geopolitical front, with the tensions in the Middle East having eased for now. The Dow has taken a run up almost to the 50,000 level again. Amazing how volatile it actually is and how fast the stock prices can move.

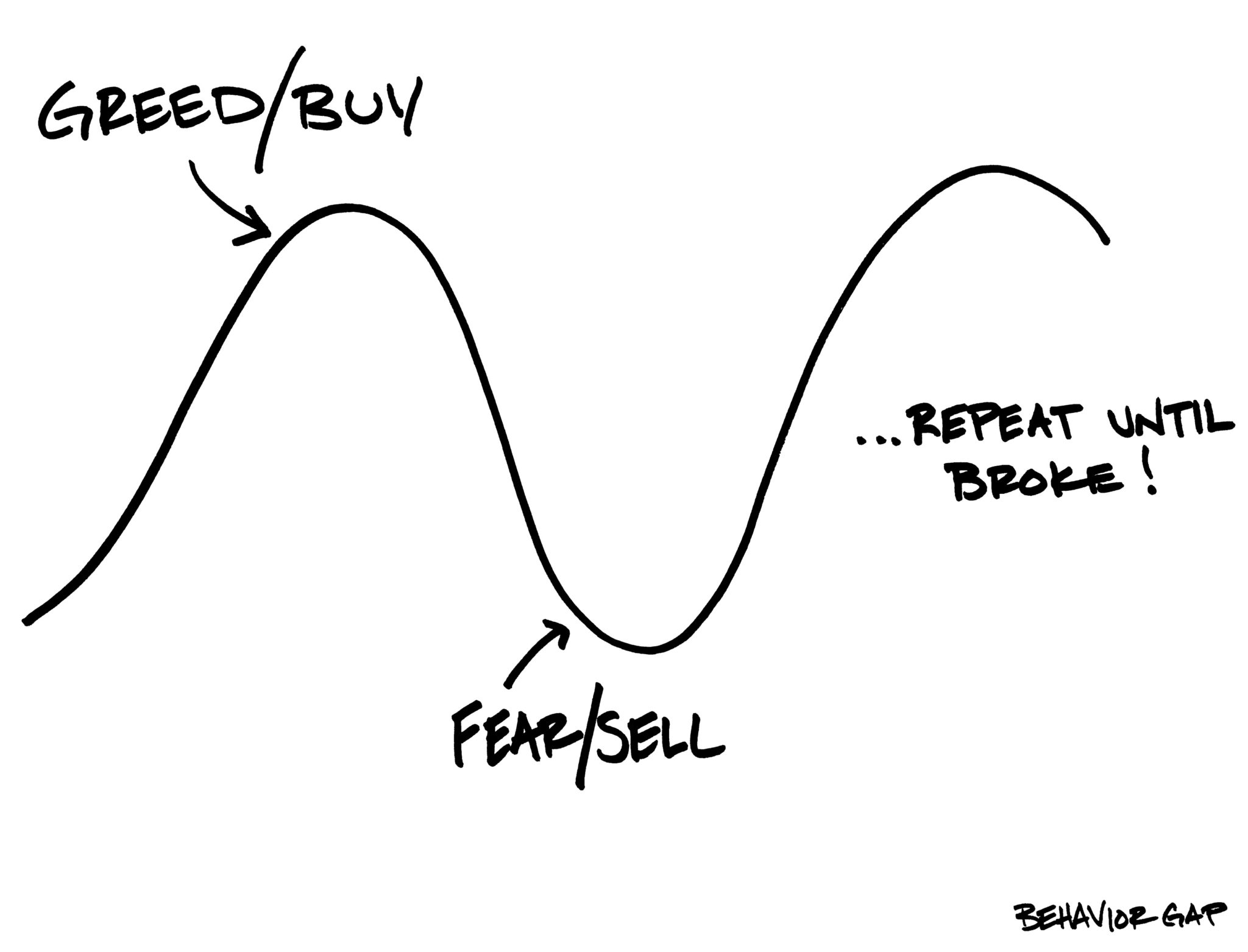

The last few months have been another lesson in how panic will destroy value. It seemed pretty bleak about a month ago as the war started, and there were fears about the ultimate strength of the Iranian regime. I’m not a politician, but it’s not clear to me that this will be another break until there is a change in the presidency and things slide the other way. What do I know?

What does all this mean for my investment strategy? As a septegenarian it’s clear. Look to remove the volatility in my portfolio and nail down some cash flows. This translates into more fixed income and more conservative stocks. A slow process, but there really is no other choice.

I did some homework and determined that an optimal annual return for me is 4%. Some investment advisors proposed that in order to achieve that goal, I should go 75% fixed income and 25% equities. I assumed an 10% annual return on my equities and 4% on the fixed income. That would give me a weighted average return of around 5.5%. They were asking for a management fee of 1%. The net to me is 4.5%. Not much margin for error, particularly in years that see a downmarket. If I simply do 100% fixed income with no fee, I have a locked-in return of 4%. I’m not sure where the investment managers are adding any value. Beats me.

Remember that the equity portion still has risk. And I’m already assuming a 10% rate of return on equities every year. This needs more work. The truth to be told is that I can live with a pretty meagre rate of return and still maintain my lifestyle. But do I need to pay so much for a little incremental return with risk?